New platforms and technologies are constantly being developed in the quickly changing world of cryptocurrencies with…

CBDC definition for Beginners: What is a CBDC?

CBDC is the government’s response to the exponential popularity of cryptocurrencies.

While there are many people who converted to using cryptocurrencies, there are those who remain mistrustful of the decentralized system. We know that government authorities have their own reservations about it too. A central bank digital currency (CBDC) is government-issued money but in its digital form. It is backed by the specific country’s fiat currency. It is the central bank that issues and oversees its distribution and usage.

The development of this new digital form of money is underway with some companies and countries partnering together to run pilot testing on the feasibility of central bank money.

Learn more about central bank digital currencies and how they can be an advantage, or disadvantage to the public and the crypto community.

Central Bank Digital Currency (CBDC) Definition

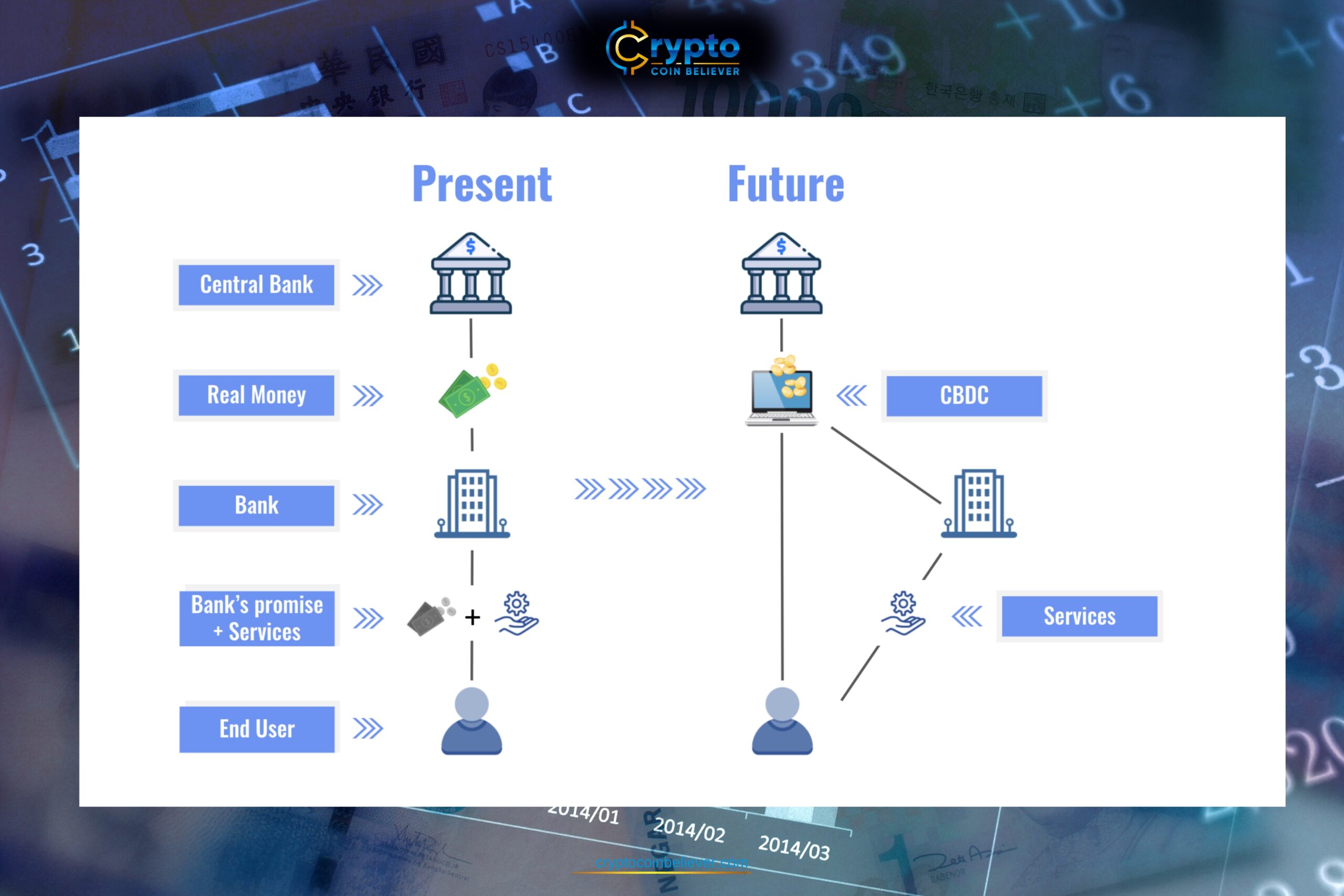

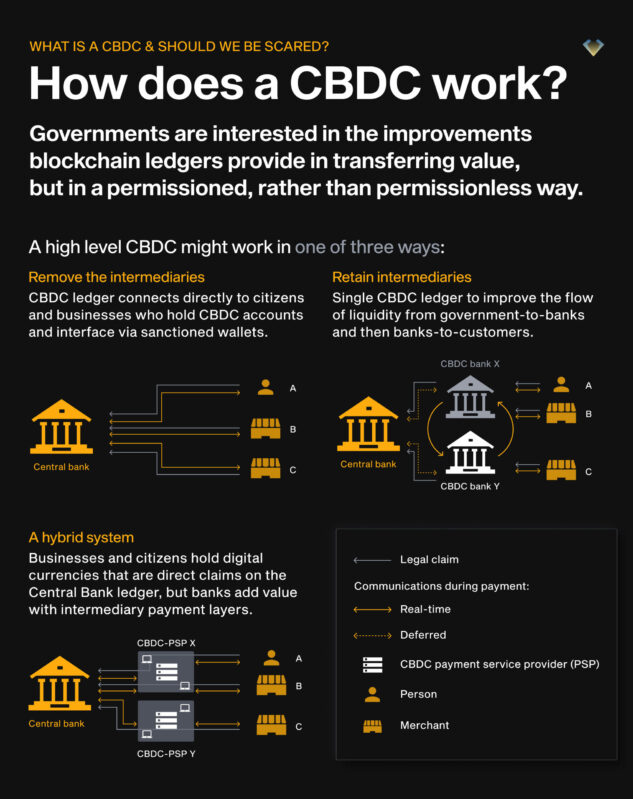

Compared to cryptocurrencies that use distributed ledger technology for its circulation and transaction validation, the CBDCs use a digital ledger for its management.

The distributed ledger technology (DLT) operates on the blockchain but a digital ledger may or may not use the blockchain technology.

Payper, a financial news site based in the Netherlands, held an interview with Harro Boven, the Dutch Central Bank policy advisor last December 2021.

According to Boven, it has three primary features: central bank issuance, digitized design and universally available to everyone.

COVID-19’s Role in CBDC Development

Physical money is still widely-used all around the world. But, when the COVID pandemic happened, there was an urgent need to shift to digital money.

The mandate of social distancing meant that people could not buy commodities and carry on their transactions face-to-face. Cryptocurrency has its issues and financial authorities believe that further developing CBDCs will help people carry on with their financial need

Aside from the coronavirus restrictions, emergency funds could not reach businesses and other intended recipients on time. Many believe that it can expedite this process in case of another emergency situation.

Types of Central Bank Digital Currency

Retail

The COVID-19 crisis gave rise to the concept of retail CBDC. This refers to central bank digital currency that users can directly hold in their own bank accounts. Commercial bank users no longer need the approval of their respective banks for emergency funds. The banks can directly deposit it into their accounts.

Retail CBDCs have two sub-categories: token-based and account-based. A token-based CBDC requires public or private keys. Also, transactions can be conducted anonymously. On the other hand, account-based needs a registered account and digital ID.

Wholesale

This is synonymous to keeping reserves in a central bank. This allows financial institutions to increase payment efficiency while reducing risks of counterparty liquidity and credit.

Many banks favor wholesale it because it has a restricted-access virtual token. If a bank owns that kind of token, they can transfer money to their recipients without third- party interference.

Central Bank Digital Currency Advantages

Easier Implementation

Wholesale CBDCs accelerate the connections between banks and CBDCs to the clients. Additionally, it lessens the work and procedures of distributing benefits and collection of taxes.

No more Intermediaries

The presence of third-parties makes centralized banks vulnerable to various risks such as cash deposits running out, bank failures, and disruptions to the system. With central bank digital currency, it uses a digital platform to improve payments.

Widespread Accessibility

CBDCs can be adjusted to function even in difficult situations such as calamities or epidemics. Transferring money will entail lower charges at a faster time which is a big help to the general public.

Central Bank Digital Currencies (CBDC) Disadvantages

Centralization

Authority still rests on a single entity- the central bank. They still have control over users’ data and all records of transactions.

Privacy

This is an offspring of the centralization problem. Service providers that the bank partners with are privy to all the sensitive information of clients. This makes CBDCs vulnerable to hacks that will exploit people’s data for criminal activities.

Country-specific regulations

Central bank digital currencies play a major role in enhancing cross-border payments. But, every government makes their legal framework about CBDCs. It is possible that conflicts will arise from the different legalities that they implement.

Countries Starting Their CBDC Development

Finland initiated their CBDC experiments in the 1990s and Venezuela, in 2018.

Based on the data from the CBDC Tracker of the Atlanta Council, a total of 105 countries have already started delving into central bank digital currencies.

Of the 105, 10 countries have formally released their own digital currencies. China will broaden the usage of digital yuan in 2023. Jamaica is the newest one to join with their JAM-DEX. Nigeria launched their own in October 2021.

On the contrary, the US and UK are falling behind in their CBDC development. This is in comparison to other G7 countries. Additionally, 19 members of the G20 have started to consider CBDC and 16 countries have already begun their pilot testing.

In the United States, there is no US CBDC yet as of March 2022.

You can see more related statistics in the Atlantic Council website.

Implications on Financial Stability

Undoubtedly, cryptocurrencies present a challenge to the fiat currencies. Moreover, because of cryptocurrencies, there are doubts about the future of the financial system.

But, it can also improve a lot of aspects about the current traditional framework. CBDC uses a unique digital ID and that will help fight off criminal elements who want to commit money laundering and fraud.

Final Word

CBDC wasn’t made to replace physical currency. Moreover, it has the power to reform the conventional financial structure. Also, CBDCs are not cryptocurrencies primarily because crypto assets are always decentralized (DeFi) but the central bank will oversee their central bank digital currencies.

It is the goal of central banks to create a back-up plan for when physical money fails, it will also reduce the need for intermediaries, and smaller holdings. Limiting CBDC holdings will not require the hassle of identification processes.

Authorities need to create a balanced design of the CBDC to be effective in initiating financial inclusion through another form of money. The current experiments that are happening will help determine the areas for improvement of CBDCs.

More to Explore

This Post Has 0 Comments